Sector Rotation Watch: Positioning for a Complex Macro Regime

The next three months present a market environment defined by tension rather than clarity. Growth remains positive but is slowing, interest rates are holding higher for longer, and inflation continues to show persistence, particularly through energy channels. At the same time, AI-driven capital expenditure and geopolitical risks are adding both opportunity and volatility. Within this backdrop, sector selection becomes critical.

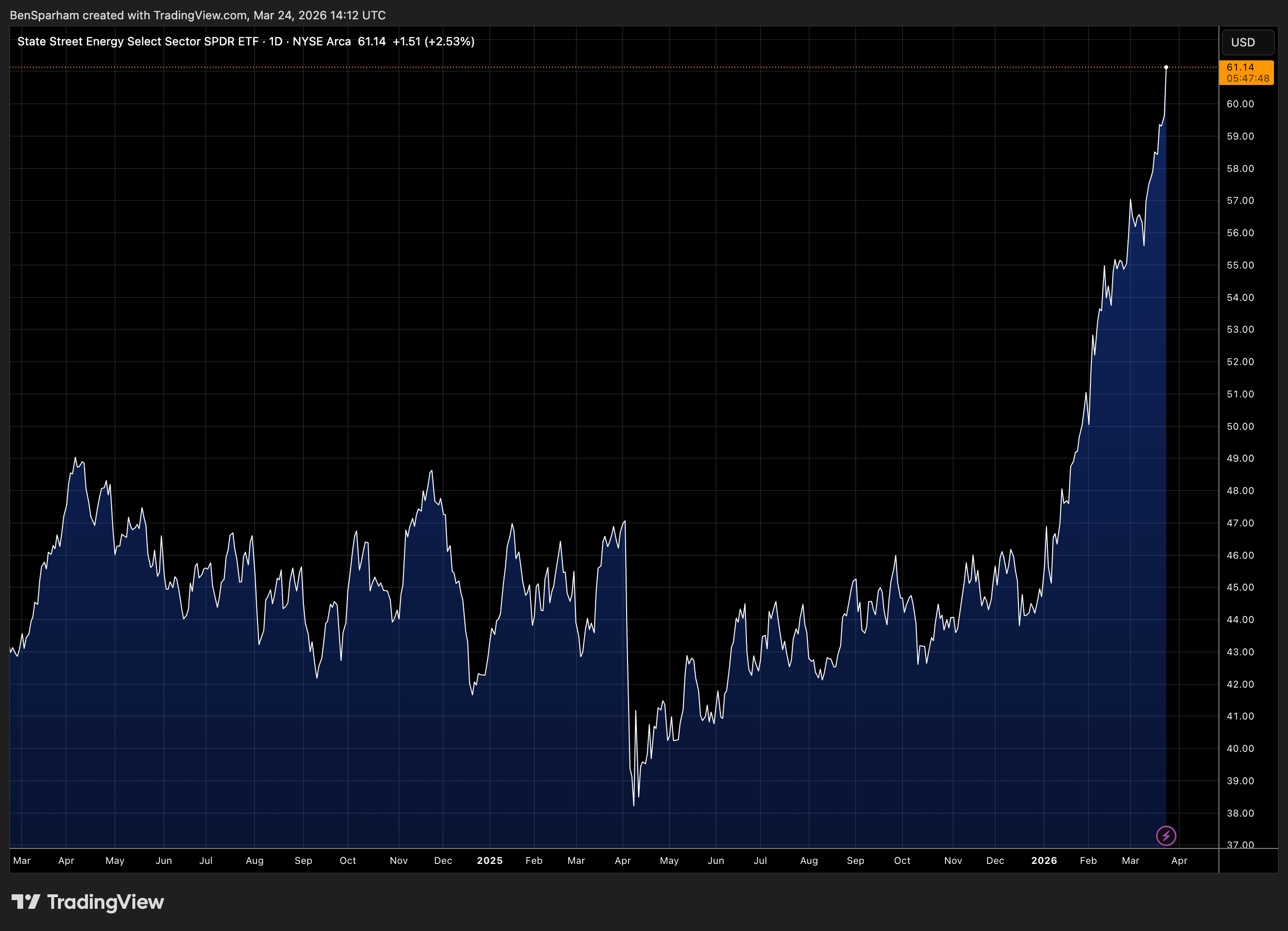

Energy and Commodities

Energy has re-emerged as a key driver of macro expectations. Recent spikes in oil and gas prices, largely tied to Middle East tensions, are feeding directly into inflation expectations and weighing on broader equity markets.

If supply disruptions persist, the setup favours energy producers and services companies with strong pricing power and robust cash flow generation. There is also a secondary effect through commodities, particularly in metals tied to infrastructure and AI demand such as copper and lithium. These areas are increasingly benefiting from structural demand rather than purely cyclical forces.

Healthcare

Healthcare continues to demonstrate its role as a defensive growth sector. Since late 2025, it has shown relative strength, supported by consistent demand and long-term demographic trends.

In a slower growth environment with elevated uncertainty, earnings resilience becomes more valuable. Healthcare offers that stability, with less sensitivity to interest rate movements compared to other sectors. The focus remains on large-cap pharma, managed care, and medical technology, alongside profitable biotech companies with clear near-term catalysts.

Industrials and AI Infrastructure

Industrials are emerging as one of the more compelling areas for earnings growth, driven by a combination of fiscal spending, onshoring trends, and the continued buildout of AI infrastructure.

The scale of investment into data centres, energy grids, and automation is significant. This is creating demand across construction, transportation, and capital equipment. Stable borrowing costs further support these capital-intensive industries, reinforcing the investment case.

Companies exposed to non-residential construction, grid modernisation, semiconductor equipment, and logistics networks are particularly well positioned to capture this trend.

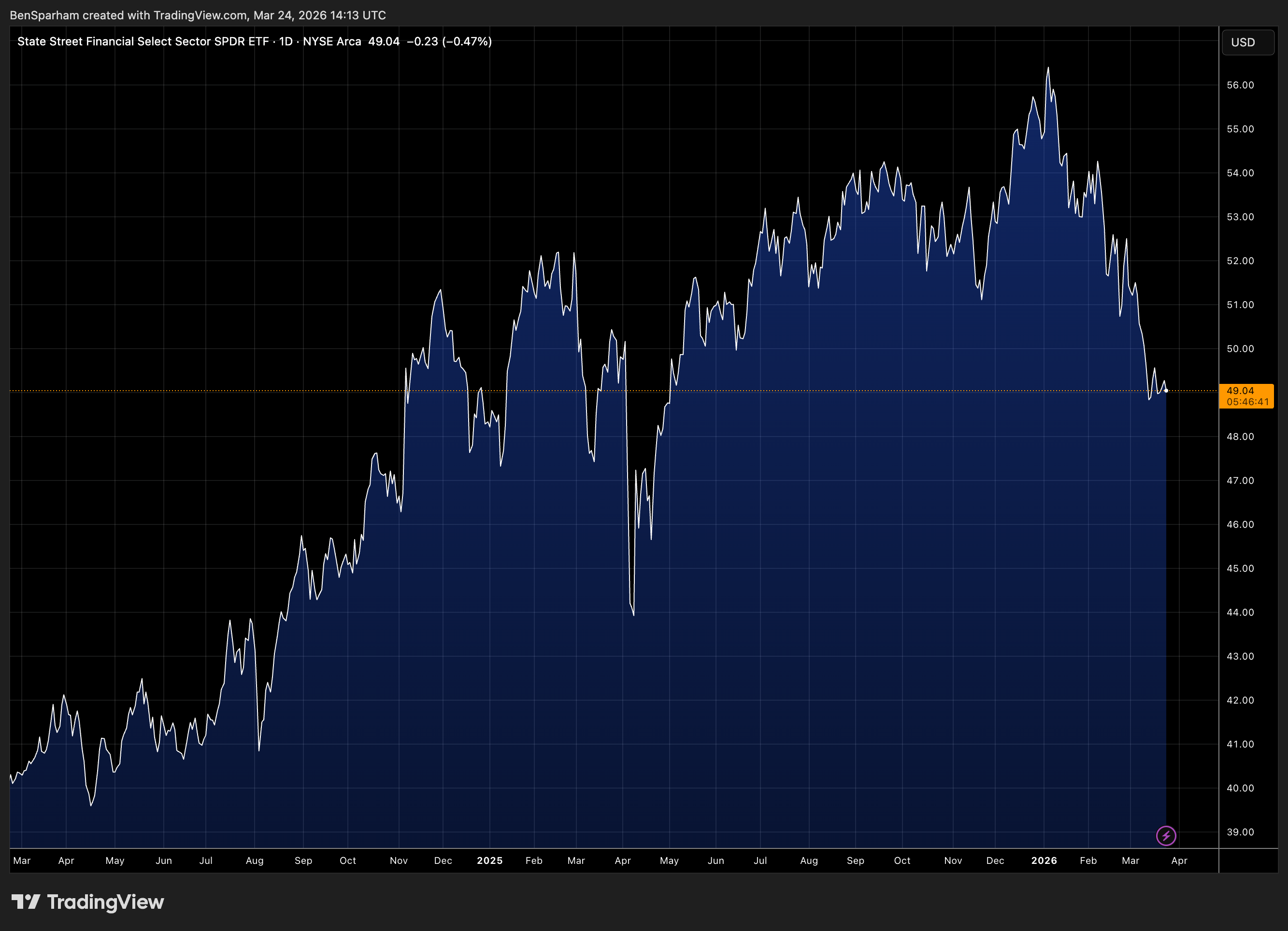

Financials and Rate Sensitivity

Despite expectations for eventual rate cuts, the current environment of elevated interest rates continues to support financials, particularly banks and insurers. Higher yields and wider net interest margins remain supportive, although this must be balanced against softer loan demand and potential credit risks.

Looking ahead, any shift towards clearer monetary easing could act as a catalyst for rate-sensitive sectors. Real estate, utilities, and cyclicals tend to respond positively to improving financing conditions, making them worth monitoring for early signs of policy repricing.

Defensives: Utilities and Consumer Staples

As growth expectations moderate, defensive sectors are attracting renewed attention. Utilities and consumer staples offer stable cash flows and dividend support, which becomes increasingly attractive in uncertain conditions.

There is also a structural layer to the utility story. The expansion of AI infrastructure is driving significant demand for power and grid investment, creating a longer-term tailwind that offsets some of the traditional sensitivity to interest rates.

Consumer staples with strong pricing power remain well positioned to protect margins against ongoing input cost and wage pressures.

Bottom Line

This is not a market driven by a single theme, but by the interaction of multiple forces. Energy is influencing inflation, AI is driving capital investment, and monetary policy remains restrictive.

In this environment, a balanced approach across cyclicals, defensives, and structural growth themes appears most appropriate. The key is not just identifying where capital is flowing today, but where earnings resilience and pricing power will persist if current conditions remain in place.